Replacement Flooring Capital Allowances

How Is Flooring Depreciated In A Rental

First Floor Demo Plan Education Design Interior Demolition Construction Drawings

Minwax Classic Gray Leap Of Faith But So Pleased Refinishing Hardwood Floors Flooring Hardwood Floors

Red Oak Floors With Classic Grey And Weathered Oak Stain Jade Floors Red Oak Floors Hardwood Floor Colors Oak Floor Stains

The Rough Black Limestone Compliments The Cream Kitchen And Dark Granite Worktops Wonderfully Kitchen Flooring Trendy Kitchen Tile Kitchen Floor Tile

Wood Floor White Walls Home House Design Home Decor

Bim46950 what is a repair.

Replacement flooring capital allowances. The implication is that floor coverings which are permanently stuck down become part of the structure of the property and therefore do not qualify for capital allowances purposes. Capital allowances are deductions claimable for the wear and tear of qualifying fixed assets such as industrial machinery office equipment and sign boards. Effect of a change of ownership. Bim46930 what is a repair.

If you want to claim capital allowances i would make a point of describing it as wooden floor covering as a substitute for carpet rather than wooden flooring. This does mean one grey area is that of stuck down carpet tiles which may be accepted by some hmrc inspectors as qualifying but possibly not by others. Replacing a whole floor covering is a whole asset contrasted with replacing some carpet tiles which is a repair. The problem is distinguishing what is a whole asset.

Character of the asset. Flooring is a little trickier because in relation to capital allowances it doesn t qualify. Bim46935 what is a repair. But if we were to simply replace the flooring e g.

Bim46925 what is a repair. Replacement expenditure is defined and brought within these new capital allowances rules to prevent some businesses from seeking to claim that they have really incurred a revenue expense on. That is what the above comments are forgetting. Replacing a whole kitchen is a whole asset and not a repair.

Bim46920 what is a repair. Any subsequent replacement of the door handle would then count as a repair of the door. Assets on which capital allowances given. The replacement of a whole asset is capital.

Bim46945 what is a repair. Better known as capital expenditures or improvements these can include big deal undertakings like carpet replacement major lighting or landscape projects pool deck refurbishment security system upgrades or replacements exterior painting painting of garages stairways or hallways and many more. Capital allowances are generally granted in place of depreciation which is not deductible. Firstly is the expenditure a repair an alteration or an improvement to the property.

Capital allowances when refurbishing a building when a property owner or tenant undertakes the refurbishment of a building there are two key questions that need to be asked in order to establish the tax treatment of the expenditure. A laminate flooring with new laminate flooring of the same quality then we would have the basis to argue it is simply a repair and then a tax reduction is available.

3451 Plywood Floor In Living Room Plywood Flooring Plywood Floor Flooring

Saratoga Hickory Laminate Planting Sequoias Attic Rooms Attic Design Attic House

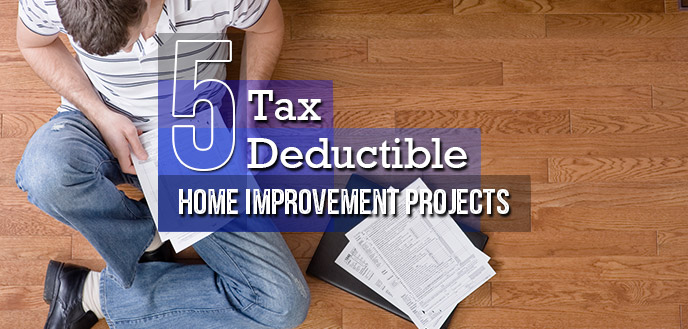

5 Tax Deductible Home Improvements For 2018 Budget Dumpster

Pin By Kelli Duke On Contractor Illustrations Kitchen Flooring Trendy Kitchen Tile Kitchen Floor Tile

Learn The Truth About Wall Ideas For Living Room In The Next 5 Seconds In 2020 Wall Decor Living Room Apartment Interior Design House Interior

Tax Breaks For Capital Improvements On Your Home Houselogic

What Is A Construction Allowance Construction Accounting

Terrazzo Flooring 5 Terrazzo Flooring Terrazzo Terazzo Floor

Ape Eternia 20x20 Bodenfliesen Fliesen Viktorianisch

Floor Area Ratio

Kitchen Countertops Diy Tile In 2020 White Granite Countertops Replacing Kitchen Countertops Kitchen Countertops

Perfect Mudroom Home Home Decor Mudroom Design

How To Depreciate Leasehold Improvements Small Business Chron Com